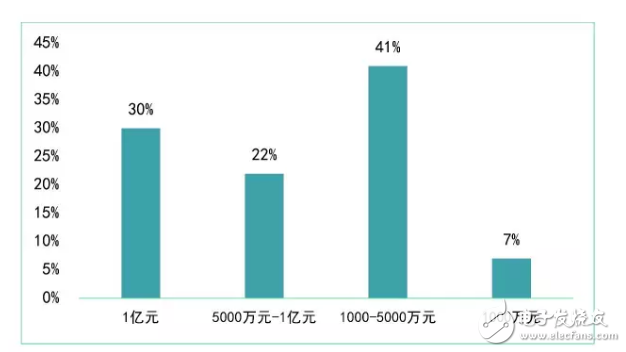

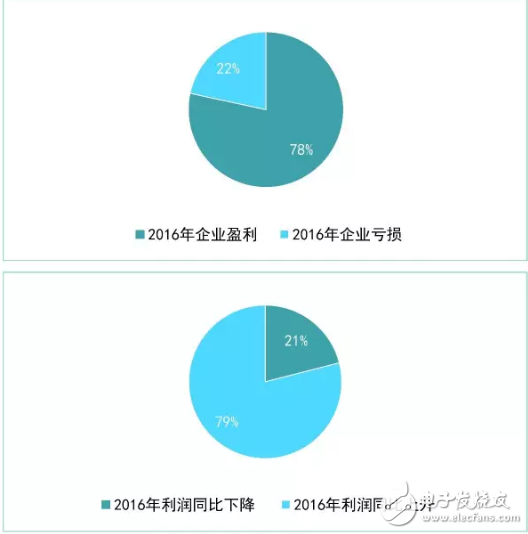

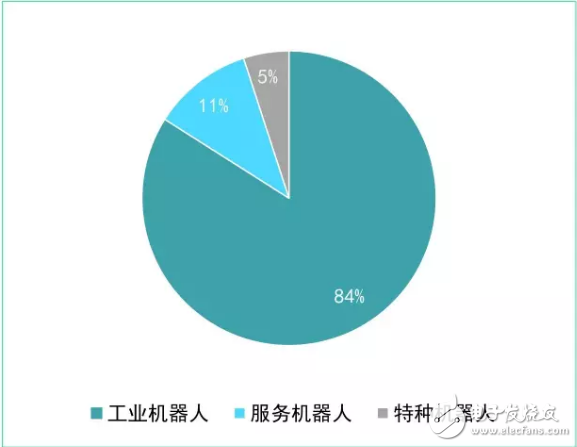

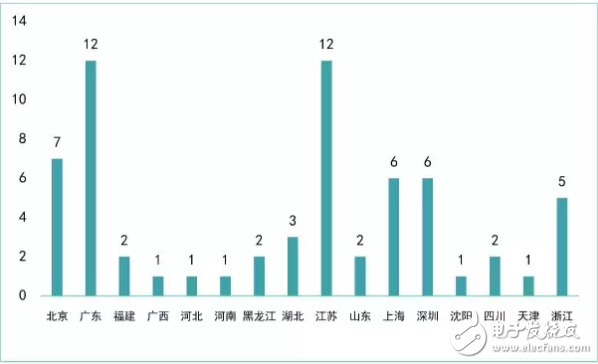

The robot industry is the jewel of the top of the manufacturing industry and a disruptive technology that leads the future. At present, the speed of China's robot industry is accelerating, and it is becoming a new kinetic energy for China's economic development. As the backbone of China's robotics industry, the new three-board enterprises are characterized by rapid development of the enterprise and the continuous expansion of the industry. They can better reflect the development status and trends of the most dynamic enterprises in the industry. This study selects the open data of 64 new robots of the New Third Board as of the end of June 2017, and systematically analyzes the development characteristics of China's new three-board robot enterprises in terms of scale efficiency, type distribution and regional agglomeration, in order to comprehensively reflect the overall development of China's robot industry. It provides a useful reference for further expanding the development space and stimulating the vitality of the industry. The scale of the enterprise is mainly small and medium-sized, and the economic benefits are significantly differentiated. Less than one-third of companies with revenues above 100 million yuan The scale of China's robot enterprises is generally small. Among the new three-board robot enterprises, the number of enterprises with revenues of 10 to 50 million yuan in 2016 is the largest, accounting for 41%, followed by enterprises with revenues exceeding 100 million yuan. 30%, the number of enterprises with revenues of 50-100 million yuan accounted for 22%, and those with revenues less than 100,000 yuan accounted for only 7%. There are still a large number of robot companies in China that have not yet been listed, and this part of the enterprises are mainly small and medium-sized enterprises. The problem of small scale and scattered quantity of Chinese robot enterprises is more prominent, and the overall competitiveness of the industry needs to be improved. Figure 1 China's new three-board robot enterprise scale Corporate losses amounted to 22% and remained stable in recent years In recent years, the overall economic efficiency of China's robotics enterprises is relatively low. In the new three-board robot enterprises, the loss of enterprises in 2016 reached 22%, which was the same as in 2015. In terms of corporate revenue, there were 17 enterprises with revenue growth of more than 20% in 2016, including 16 industrial robot companies and 1 service robot company. The company with the highest year-on-year growth in revenue is Zhisheng Intelligent, with a growth rate of 90%, indicating that the service robot enterprises in key segments have great development potential; 8 companies with a year-on-year decline in revenues of more than 20% in 2016, including 5 Industrial robot companies, two service robot companies and one special robot company, the company with the highest year-on-year decline in revenue was the finder company, with revenue falling by 66% year-on-year. In terms of corporate profits, in 2016, 79% of corporate profits increased year-on-year, and 21% of corporate profits fell year-on-year, indicating that the development of robotics in 2016 has a general trend. Figure 2 Profitability of China's new three-board robot companies Entrepreneurial abilities in key development areas China's robotics enterprises are favored by the capital market. In the field of industrial robots, the core key technologies are mastered by foreign leading enterprises. The development of traditional fields is limited. The emerging markets such as robotic arms and other capital markets have high attention and the development momentum of enterprises is full. For example, Shenzhen Sinus Electric Co., Ltd. is mainly engaged in the field of mechanical arms. In 2016, the profit was more than three times that of 2015, leading the overall new three-board robot enterprise. In the field of service robots, the key segments of medical robots and virtual robots have large capital investment, and the enterprises have expanded rapidly, mainly investing in future development expectations, showing the characteristics of rapid profit growth and an increase in the actual loss of enterprises. For example, Tianzhihang is the only listed surgical robot in China. In 2016, its profit increased by 80% year-on-year, while the losses in 2016 and 2015 reached 25 million and 14 million. As the only virtual robot listed company in China, Zhisheng Smart has a 90% year-on-year revenue growth in 2016, while losses in 2016 and 2015 totaled 71 million and 65 million. Industrial robot companies account for the highest proportion and complete industrial chain China's robotics companies are mainly industrial robots. Among the new three-board robot companies, industrial robot companies account for 84%. Among them, the industrial robot industry is relatively mature, the industrial chain is complete, the middle and lower reaches are complete, but the distribution is slightly uneven. There are more upstream and downstream enterprises and fewer midstream enterprises. Among them, the typical industrial robot industry chain upstream enterprises are Huaheng, Beichao Servo, Xingchen Technology, Sinus Electric, Jiale, Gaojing CNC, Lechuang Technology, Dingju Technology, Jiechuang Technology, Dayuan Shares, Taizhou Motor, Linkman, and Yinfeng shares; the main industry chain involves the manufacture of ontology, with high thresholds. The main enterprises include supersonic and Ford shares; the downstream enterprises in the industrial chain mainly focus on system integration, focusing on application scenarios, mainly There are Bronte, Wodi equipment, Mingsai Technology, Haiwei Intelligent, Jiayi Precision Machinery, Kunming Robot, Shunda Intelligent, Hengxin Intelligent, Jiangsu Beiren. Figure 3 Distribution of product types of new three-board robot enterprises in China Service robotics companies focus on medical, virtual and professional services Among the new robotics companies in China, the number of service robots accounts for 11%, and the vast market and consumption upgrades will support the development of enterprises. Among the new three-board robot companies, the service machine enterprise type is very focused, mainly involving medical robots, virtual robots and professional service robots. Among them, medical robots and virtual robots have only one listed company, indicating that compared with industrial robots, service robots started late, and with the continuous development of this field, the number of listed companies will further increase. The field of professional service robots, with cultural exhibition robots, cleaning robots, cooking robots, drones, underwater robots and kitchen robots, shows that such subdivisions are the earliest areas for service robots to enter the market, and have gradually formed mature markets. Sub-field “small giants†began to take shape, and the industrial structure and industrial scale are continuing to grow. Special robots focus on pipeline and air duct detection robots China's special robots account for a relatively small proportion of new three-board robot companies, accounting for only 5%, but still have a certain development momentum. The new three-plate special robots are concentrated in the field of pipeline inspection and air duct detection, while the widely used security robots, explosion-proof robots, anti-terrorism robots, and underwater robots in special robots are concentrated on large-scale mainboard companies such as CITIC Heavy Industries, Xinsong and Helen. Zhe et al. indicate that the application market concentration in such fields is relatively high. The application scenarios for pipeline inspection and air duct detection are very clear, and it is a field of special robots that has developed rapidly in recent years. Among the new three-board robot enterprises, there are two pipeline inspection robot enterprises, namely Longkexing and Zhongyi, respectively. Among them, Longkexing has a large scale, and its revenue in 2016 exceeded 100 million yuan. The new three-board robot enterprise is only one of the wind tunnel testing companies in Beijing. The company's revenue in the first half of 2016 was nearly 10 million yuan, and the net profit was 240,000 yuan. This indicates that the market for wind tunnel testing is narrow, and the special robot products of large-scale mainboard listed companies are still It does not involve this field and has a relatively high concentration of enterprises. The distribution of enterprises is concentrated in the Pearl River Delta, the Yangtze River Delta and Beijing-Tianjin-Hebei, and the regional agglomeration effect is remarkable. Guangdong, Jiangsu and Beijing occupy the top three new three-board enterprises From the perspective of the number of new three-board enterprises, three echelon teams have been formed. Guangdong and Jiangsu rank first in the echelon (more than ten), and Beijing, Shanghai, Shenzhen and Zhejiang rank second in the echelon (more than five in less than ten). The provinces and cities are ranked third (less than five). Based on various industrial agglomeration areas, the Pearl River Delta region (12 in Guangdong, 6 in Shenzhen), the Yangtze River Delta region (12 in Jiangsu, 5 in Zhejiang), Beijing-Tianjin-Hebei region (7 in Beijing, 1 in Tianjin, 1 in Hebei) These three regions are the first-mover advantage areas of China's robot industry, while the Northeast region (2 in Heilongjiang and 1 in Shenyang) has the basis of traditional industrial robots. The central and western regions (3 in Hubei, 2 in Sichuan, 1 in Henan, and Guangxi) 1) is a post-development area in the robotics field, but the pace of development is accelerating. Figure 4 Regional distribution of China's new three-board robot enterprises (unit: home) Development of industrial robots in the Yangtze River Delta and the Pearl River Delta, Beijing-Tianjin-Hebei mainly serves and special robots From the perspective of the product types of the new three-board enterprises, the Yangtze River Delta region, the Pearl River Delta region and the Northeast region are mainly industrial robots. The Beijing-Tianjin-Hebei region focuses on the development of services and special robots. Among the new three-board robot enterprises, only one of Jiangsu's 12 companies is a service robot, and the rest are industrial robots; only one of Shanghai's six is ​​a service robot, and the rest are industrial robots; five of Zhejiang's enterprises are industrial robot enterprises; All enterprises are industrial robot companies; two of the three companies in Heilongjiang and Shenyang are industrial robot companies. In contrast, in the Beijing-Tianjin-Hebei region, there are 2 service robots and 2 special robots among the 12 companies in Beijing. The only medical robot listed company in the country is located here. On the whole, although industrial robots and service robots have different levels of location, in the areas where industrial robots are developed, there will be a small number of powerful service robots, such as virtual robots, which are deployed in Shanghai. The Yangtze River Delta and Pearl River Delta industrial chains are relatively complete, and Beijing-Tianjin-Hebei key development industry upstream From the distribution of the industrial chain of the new three-board enterprises, in the field of industrial robots, there are many upstream and downstream enterprises in the Yangtze River Delta region, and the Pearl River Delta industry has the highest efficiency, and the Beijing-Tianjin-Hebei industrial robots are mainly upstream industries. Among the typical enterprises with large scale of the new three-board in China, there are 4 upstream of 3 upstream of Jiangsu; 1 upstream of Shanghai, and Vodi as the downstream leading enterprise; 3 downstream of 3 downstream of Guangdong; 2 upstream faucets of Beijing Enterprises, respectively, are Beichao Servo and Linkman. In the field of service robots, Guangdong has the most complete industrial chain, which benefits from the leading level of industrial support in the intelligent hardware field in Guangdong Province, while the Beijing-Tianjin-Hebei region, especially Beijing, is the central area of ​​national intelligent technology in image recognition and speech recognition. The development of artificial intelligence is second to none, and the industry level is significantly higher than other major regions in the country.

Description: motherboard,mainboard,asus-motherboard,motherboard price Easy Electronic Technology Co.,Ltd , https://www.pcelectronicgroup.com

The 847-Pro Mining Motherboard is a basic motherboard that supports 20 graphics cards, the boards used for Ethereum and other less resource-intensive scripts. The cards connect via PCIe-over-USB and each port has is individually controlled and managed by on-board diagnostics.

Support 1660, 2070, 3090, rx580 and other full series of graphics cards.

Support common mining cards, such as: RX series, GTX10 series, gtx20 series, gtx30 series, etc.

This motherboard has a large display card pitch of 65mm, which is more stable without switching.

The

motherboard adopts HM65 chip, all solid capacitors, gigabit network

card, integrated notebook CPU, DDR3 notebook memory slot.