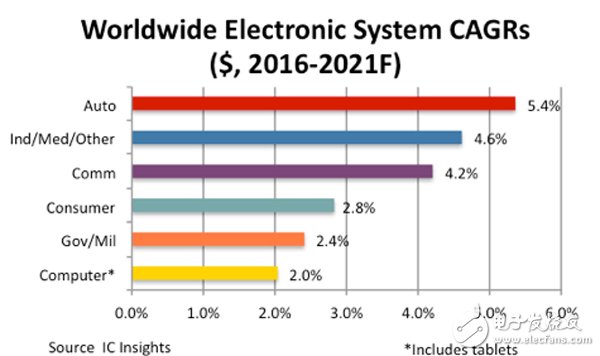

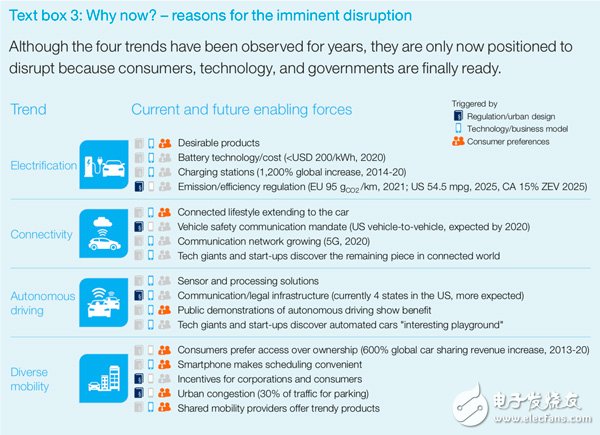

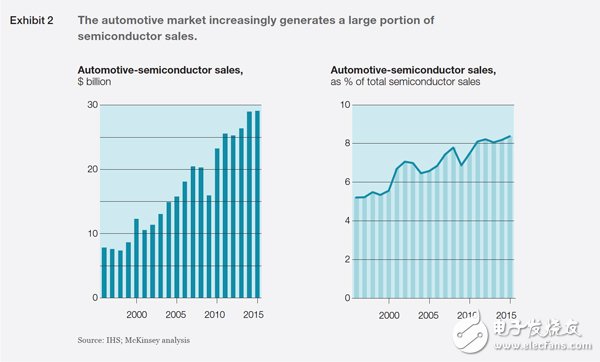

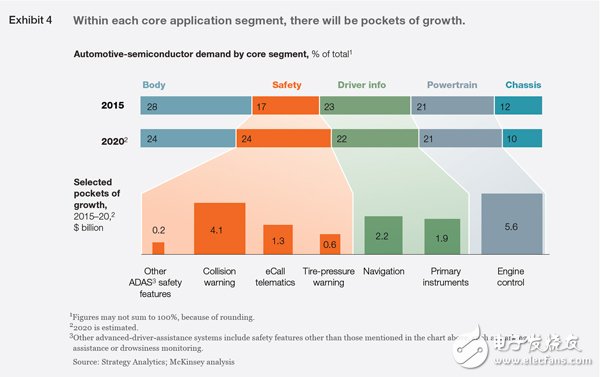

ZTE has been banned and the opportunity of China's auto chip company has come. ZTE’s “core†and China’s “chip weakness†were once again exposed. Focusing on the development of the automotive chip business, in recent years, when the performance of the PC semiconductor market has declined year by year, automotive semiconductors have maintained a sustained high growth momentum. According to market research firm IC Insights, by 2021, automotive semiconductors will become the strongest terminal market in the chip industry, and the CAGR of sales of automotive electronic system products will achieve a 5.4% increase. Global electronic system annual compound growth rate The reason is that the demand for the number of electronic systems inside the car is constantly rising. More and more car companies, suppliers and technology companies have turned their attention to the realization of auto-driving, V2V/V2I and other car networking functions, while national automakers are gradually increasing R&D investment in electric vehicle technology. Because semiconductors are key components driving the vast majority of automotive innovations, including vision-based enhanced graphics processing units (GPUs), application processors, sensors, and DRAM and NAND flash. As the complexity of automobiles increases, the demand for automotive semiconductor components is bound to grow steadily. Therefore, the automotive sector is a new engine for the semiconductor industry to promote its long-term development. Although the car accounts for only about 10% of the entire chip industry compared to other sectors, Gartner Group predicts that by 2020, the profit growth rate of the automotive semiconductor business segment will be global chips. Double the market. Then, at the time of the ZTE incident, it is appropriate to talk about the rapidly emerging automotive chip market and the opportunities for differentiation of Chinese auto chip companies in the development of their own brand “new fourâ€. Evolving car market To be honest, the automotive industry has never experienced so many simultaneous changes. In the past few years, we have witnessed the integration of a large number of new technologies into mass-production models, including matrix LED headlights, lidar sensors and continuously optimized camera sensors. Of course, technologies such as 3D map applications, electric vehicle batteries, and augmented reality have all improved, and 5G communication networks and next-generation travel solutions may soon become a reality. In addition, consumers' preferences and attitudes toward cars are also changing. For example, the number of customers who have the idea of ​​“buying a car is important†continues to decline. A report issued by consulting firm McKinsey pointed out that by 2030, the global automotive industry will mainly change in the following four directions: In the next 10 years, as battery prices continue to decline while the number of charging infrastructure increases, by 2020, the number of electric vehicles will account for 5% to 10% of new car sales. Taking into account changes in the level of technological progress, the form of government regulation, and the rise and fall of electricity prices, the proportion of new electric car sales will fluctuate between 35% and 50% by 2030. Whether a car has interconnected functions is strongly affecting consumers' choice of car purchases, and may have a greater impact on their decisions in the future. In 2016, McKinsey found that 41% of respondents reported turning to other new car brands for better connectivity. At the same time, consumers in each country have different levels of awareness of this matter, and 62% of Chinese consumers believe that connectivity will be a decisive factor in their car purchase. In contrast, US and German consumers holding the same view accounted for 37% and 25%, respectively. Correspondingly, the interconnection sector will bring huge profits to car companies. By 2020, it is expected to soar from the current 30 billion US dollars to more than 60 billion US dollars. Although car companies are gradually introducing more ADAS functions into production cars, high-automatic vehicles that can reach Level 4 are expected to be on the road as early as 2020-2025. After that, the number of mass-produced unmanned vehicles will show steady growth. In 2030, 35% of Level 3 autopilots are expected to be on the road, and 15% will be Level 4. However, the effect of commercialization of autonomous driving can be achieved. The factors that restrict it include the evolution of core technology, price, consumer acceptance, and the ability of OEM/parts suppliers to assess and respond to possible security risks. Although the per capita car ownership rate in developed countries is increasing year by year, with the rapid travel of shared travel and car sharing and network car service, the car ownership rate will slow down or stagnate in the future. Take the North American market as an example. The number of consumers joining the car sharing service has increased by 400% between 2018 and 2015, and this number is expected to reach a new high in the future. According to McKinsey analysts, by 2030, online car or travel sharing services will account for 10% of new car purchases. This trend has also prompted many car companies to share in the travel sector, so as not to lag behind other competitors. With the readiness of consumers, technology and government, these four trends will dominate the global automotive industry in the future: McKinsey & Company The changes in the four global automotive industries mentioned above will have a major impact on the differentiation and growth of the entire industry. At the same time, the growing income from travel and enhanced connectivity services is probably the most dramatic change. But the impact of these four major trends is not single, they will also promote the development of other areas. For example, the price of autonomous vehicles (L3/L4) is very high, which will lead to a rise in the profit of new car sales. In the aftermarket segment, the introduction of new travel services will help increase the profitability of this business segment, as shared cars face higher maintenance costs. However, the aftermarket is also facing the risk and pressure of falling profits, because the powertrain system of electric vehicles is cheaper than the repair of fuel vehicles. Even a self-driving car with a collision accident may be better than the same ordinary fuel vehicle. The cost is as low as 90%. Of course, whether it is ups and downs, the wave of “four transformations†that the auto industry is experiencing will have an impact on the demand for semiconductors and other parts companies. The value of the automotive semiconductor market in the past and the future Despite the possible uncertainties, Che Yun believes that with the increasing demand for safety, comfort and connectivity in the automotive industry, the automotive semiconductor market will continue to grow in the medium and long term. In particular, the rapid development of autonomous driving technology will aggravate this trend. In the long run, electric vehicle-related products will also see significant growth, because hybrid models contain $900 worth of semiconductors, while ordinary pure electric vehicles carry more than $1,000 worth of chips, which is far more than the average of 330 in traditional internal combustion engines. The use of US dollar semiconductor products is much higher. During the two decades from 1995 to 2015, semiconductor products sold to automakers increased from the initial $7 billion to $30 billion. Because of this high growth rate, sales of automotive semiconductor products account for about 9% of the total sales of the entire semiconductor industry. Judging from the current growth trend, sales of automotive semiconductor products will continue to rise during the period from 2015 to 2020, resulting in a 6% increase. The entire semiconductor industry is expected to increase sales by only 3% to 4% during the five years. Therefore, the annual sales of automotive semiconductors may achieve a breakthrough in the range of 39 billion to 42 billion US dollars. Although there are many opportunities for automotive semiconductor manufacturers in the future, Che Yun believes that different companies have different developments due to different regions, automotive applications and different equipment divisions. Regional growth: a new impetus for the automotive semiconductor industry Although the US and European markets still dominate, the annual sales growth of automotive semiconductor products in the Chinese market is leading the world. The average increase was 15% between 2010 and 2015. Some analysts expect that China's auto semiconductor market will continue to occupy the top position in sales growth by 2020. However, due to the slowdown in national economic growth and the surge in automobile sales, the average revenue is expected to decrease by 10%. Changes in market demand due to device and application segmentation In addition to studying trends in different geographies, Che Yun also explored the possible impact of core automotive applications and different device classifications on automotive semiconductor market demand. Current core automotive semiconductor applications are concentrated in the following areas: safety, powertrain, body, chassis and driver information. And there is a trend to show that by 2020, the fastest growing segment will be in the security arena. In each core application area, some products may achieve higher speed growth than other categories. For example, in the security field, the compound annual growth rate (CAGR) of collision warning system products is expected to reach 22% between 2015 and 2020, while sales will increase to $4.1 billion. And from the long-term development trend after 2020, engine control applications (including electric motors and power electronics) are expected to achieve sustained growth. In addition, like the sensor fusion technology required for L4 level autopilot and the ECU in the integrated control system, the integrated system solution products similar to the above are expected to achieve higher and faster growth. The semiconductor market demand can be divided into different devices: memory, micro components, logic devices, analog devices, optical devices, sensor devices and discrete devices. By the time 2020, the number of electric vehicles in the world will surge, and in addition to the number of semiconductors required in the car far more than the traditional models, electric vehicles also need different types of automotive semiconductor products, which will cause the market supply and demand mode to occur. Variety. For example, up to 10% of automotive semiconductors used in conventional cars will be integrated into discrete devices (power electronics). In contrast, 30% to 40% of automotive semiconductors in hybrids are discrete devices, while other electric vehicles account for up to 50%. Although electric vehicles will not be widely favored by consumers until around 2020, sales of electric vehicles have shown an upward trend. This means that the market demand for automotive semiconductors will also begin to change. Similar to the core automotive applications sector, each semiconductor device segment will usher in a number of opportunities to make money. For example, for micro-component products, the compound annual growth rates of micro-component products used in microprocessors, MCUs, and digital signal processors are 14%, 9%, and 3%, respectively. After 2020, Strategy AnalyTIcs and McKinsey analysts expect all core business to continue to grow. However, as autonomous driving and electric vehicles are increasingly favored by the industry, their related applications (GPUs, sensors, etc.) are bound to perform much better than other product market prospects. Strategic issues & what to do next? 1 How to differentiate products? Most of the top semiconductor companies in the industry have mentioned that placing products and R&D centers on hardware does not bring ideal value to the ever-changing automotive industry. Therefore, most companies hope to provide system solutions by adding software algorithms to their products. Some companies choose to cooperate to differentiate products. For example, Nvidia announced that it will continue to work with map supplier HERE, which will jointly develop real-time, high-precision maps for self-driving cars. Intel also said it will build the Intel GO Auto 5G platform, which allows automakers and TIer 1 suppliers to validate designs around 5G. Suppose semiconductor companies focus on products such as system solutions and no longer develop additional stand-alone chips. The benefit is that they can avoid the growing financial pressure. For example, Dutch semiconductor company NXP released a SAF4000 fully integrated software radio solution for IVI, an in-car entertainment information system, last year. NXP said "This is the world's first single-chip system that covers all radio standards worldwide, including AM/FM, DAB+, DRM(+) and HD." 2 Does the life cycle of semiconductors in the car change? In the future, as long as a car is still on the market, we may find that the frequency of car manufacturers buying chips will increase dramatically. And if an optional feature like IVI is no longer bundled with other applications related to other hardware updates (such as powertrains), then this change will be rapidly evolving. 3 How high integration is required to ensure material cost while ensuring redundant design? Some semiconductor companies are trying to turn the chip system into an integrated unit to ensure redundancy by adding multiple MEMS, MCUs and other sensors. But we must first understand the concept of "redundancy", which means adding two or more key components or functions in a system to increase the security of the system. For example, redundancy is primarily used for backup or fault protection. There may be a host factory that finds a specific redundant design that can improve chip performance, such as adding more ECUs. There are also some that explore the use of electronic remote control to manipulate the brakes or steering. So the question is, how much redundancy can ensure the safety of the car? And when will the participants in the automotive industry be assured of products with less redundant design? These are all key issues that limit the cost of the chip. 4 How should semiconductor companies work with automakers and TIer 1 suppliers? At present, there is more and more direct cooperation between semiconductor companies and car companies and suppliers. For example, BMW, Intel and Mobileye have announced that they will cooperate to build a 40-seat autopilot test fleet; similarly, Audi's new A8 model launched last year is equipped with a set of zFAS domain controllers, including Intel, NVIDIA, and Mobileye. Different chips are provided to solve the problem of automatic driving in highways and traffic congestion scenarios. Audi and Nvidia have reached a cooperation at the CES International Consumer Electronics Show in 2017. The two sides will jointly develop artificial intelligence vehicles and plan to achieve commercialization in 2020. Of course, in order to cooperate successfully, semiconductor companies must first determine the scope of cooperation within which the technology or products of the two companies can complement each other. Then the two sides can explore the form of cooperation: mergers and acquisitions, joint ventures, exclusive partnerships or strategic partnerships? In the end, it is always necessary to negotiate in the direction of the interests of both parties. 5 What direction will the global automotive industry change in the future? What impact will such changes have on semiconductor companies? Changes in competitive domains and value chains can affect the future development of major semiconductor companies. Some leading OEMs may also occupy half of the global market in the future, and those companies that have long been eyeing the mass market will gradually lose some profits with the rise of some new Chinese companies. ICT (information and communication technology) providers in other countries will clearly feel the rising demand for their products, including sensors and software, which will make them play an important role in the value chain. In the end, some TIer 1 car suppliers can even bargain with some non-primary car companies. 6 How far does automotive semiconductor suppliers go on the issue of “securityâ€? Although it is critical for semiconductor companies to integrate security functions into the chip, it is not necessarily a once-and-for-all solution to all security issues. For example, security risks associated with hacking. Therefore, they need to develop other security solutions, especially in the area of ​​automotive interconnects that are easily overlooked. Some semiconductor suppliers such as NXP have begun to develop end-to-end security solutions with partners in the automotive industry, and other companies can learn from their cooperation models. In addition, semiconductor companies can find inspiration in other high-tech companies with innovative product outputs. For example, Bosch has previously introduced a keyless entry and start-up engine that allows drivers to enter the car in a safe manner, which requires only a fully encrypted smartphone. 7 How to evaluate the development of China's automotive semiconductor market? Semiconductor companies need to look at the Chinese market from several different perspectives. In addition to the continued rise in demand for automotive semiconductor products in the Chinese market, it will also be one of the major markets for autonomous driving tests and high levels of electric vehicle ownership. Part of the reason for this judgment is that China's consumer market has several special places. According to a survey released by McKinsey in 2016, among the more than 3,000 respondents from China, Germany and the United States, consumers in the Chinese market have an attitude toward V2V technology compared to the other two countries. More open. At the same time, they are more willing to use OTA to upgrade their car entertainment information system. All of the above reasons may encourage and encourage car companies to test and market the main battlefield of new car technology in China, especially in recent years, China's domestic car ownership is steadily rising. In addition, the Chinese market provides a large number of differentiated cooperation opportunities for semiconductor companies. At the CES International Consumer Electronics Show in the past two years, Chinese companies have contributed more than 1,300 exhibits, accounting for more than 20% of the 500 exhibits related to automotive technology. In the United States and other countries, there are also some potential partners, who are often Chinese companies that have just been involved in the automotive field. For example, China's local search giant Baidu is trying to develop autonomous driving and electric vehicle technology through cooperation with global companies. It should also be pointed out here that semiconductor companies should have confidence in the Chinese market, both at the market level and from the perspective of partner channels. With the proposal and implementation of the "Made in China 2025" strategy, analysts expect that the Chinese government will introduce relevant preferential policies and measures in the future to support local production and manufacturing. For example, if a Chinese local company wants to upgrade its production line and increase the research and development of innovative technologies, it will receive a series of preferential policies and financial support from the Chinese government. Therefore, semiconductor companies may find that there are more and more potential partners in the future. At the same time, the Chinese government has shown great interest in autonomous driving and electric vehicle technology, and technologies such as the Internet of Things related to smart connected cars are also one of the nationally supported projects. At present, with the support of the government, more and more automobile and ICT manufacturers have shown very strong development momentum in the Chinese market. The reality is that while many semiconductor companies are rapidly investing in the development of innovative automotive products, and as a top supplier in the field of autonomous driving and electric vehicles, other industry players are slow to establish cooperation with automakers. Or invest in the core technology that car companies pay attention to. A big part of the reason is that they may not be willing to risk investing too much in a market that has not yet formed and is still changing rapidly. But the problem is that these relatively conservative companies have repeatedly hesitated and may soon be taken away by aggressive competitors. As the automotive market is increasingly driving the growth of the semiconductor industry, inaction is actually the biggest risk facing the company.

Power Meter is a monitoring and testing instrument which determines the power consumption of a connected appliance and the cost of the electricity consumed. Power meter socket, Energy meter socket, Energy meter cost socket, Power meter cost socket, Energy power meter socket NINGBO COWELL ELECTRONICS & TECHNOLOGY CO., LTD , https://www.cowellsocket.com

Recently, the US Department of Commerce announced that it will ban US companies from selling any electronic technology or communication originals to China ZTE in the next seven years. For ZTE, the devastating blow is not only its traditional business, but also its intelligent networked car business, such as automotive chips and operating systems.

Built-in 3.6V rechargeable Batteries ( . The purpose of the batteries is to store the total electricity and memory setting

Resetting

If an abnormal display appears or the buttons produce no response, the instrument must be reset. To do this,

press the RESET button.

Display Mode

Entire LCD can be displayed for about 1 minute and then it automatically gets into Model. To transfer from

one mode to the other, press the FUNCTION button.

Mode 1: Time/Watt/Cost Display Display duration(how long) this device connect to power source.LCD on first line shows 0:00 with first two figures mean minutes(2 figures will occur while occur at 10 min) and the rest shows seconds. After 60mins, it displays 0:00 again with first two numbers meas hour(2 figures will occur at 10hours)and the rest shows minutes. The rest can be done in the same manner which means after 24 hours, it will re-caculate. LCD on second line displays current power which ranges in 0.0W 〜 9999W. LCD on third line displays the current electricity costs which ranges in O.Ocost 〜 9999cost. It will keep on O.OOcost before setting rate without other figures.

Mode 2: Time/Cumulative electrical quantity Display Display duration(how long) this device connect to power source.

LCD on first line shows 0:00 with first two figures mean minutes(2 figures will occur while occur at 10 min) and the rest shows seconds. After 60mins, it displays 0:00 again with first two numbers meas hour(2 figures will occur at 10hours)and the rest shows minutes. The rest can be done in the same manner which

means after 24 hours, it will re-caculate. LCD on second line displays current cumulative electrical quantity which ranges in 0.000KWH 〜 9999KWH without other figures. LCD on third line displays"DAY"- "1 'Will be showed on numerical part(the other three figures will be showed at carry) which means it has cumulated electrical quantity for 24hours(one day). The rest can be done in the same manner untill the maximal cumulative time of 9999 days.

Mode 3: TimeA^bltage/Frequency Display LCD on first line displays the same as Mode 1 dones. LCD on second line displays current voltage supply (v) which ranges in 0.0V 〜 9999V .LCD on third line displays current frequency (HZ) which ranges in 0.0HZ 〜 9999Hz without other figures.

Mode 4: Time/Current/Power Factor Display LCD on first line displays the same as Mode 1 dones.LCD on second line displays load current which ranges in 0.0000A 〜 9999A. LCD on third line displays current power factor which ranges in 0.00PF 〜 LOOPF without other figures.

Mode 5:Time/Minimum Power Display LCD on first line displays the same as Mode 1 dones. LCD on

second line displays the minimum power which ranges in 0.0W 〜 9999W. LCD on third line displays character of "Lo" without other figures.

Mode 6: Time/Maximal Power Display LCD on first line displays the same as Mode 1 dones. LCD on second line displays the maximal power which ranges in 0.0W 〜 9999W. LCD on third line displays character of "Hi" without other figures.

Mode 7: Time/Price Display LCD on first line displays the same as Mode 1 dones. LCD on third line displays the cost which ranges in O.OOCOST/KWH 〜 99.99COST/KWH without other figures.

Overload Display: When the power socket connects the load over 3680W, LCD on second line displays the''OVERLOAD[ with booming noise to warn the users, (selectable choice)

Supplemental informations:

1: Except [OVERLOAD[ interface, LCD on first line display time in repitition within 24hours.

2: LCD on first line, second line or third line described in this intruction take section according to two black lines on LCD screen. Here it added for clarified purpose.

3. Mode 7 will directly occur while press down button "cost".

4. [UP"&"Down" are in no function under un-setting mode.

Setting Mode

1. Electricity price setting

After keeping COST button pressed lasting more than 3 seconds(LCD on third line display system defaults price, eg O.OOCOST/KWH ),the rendered content begins moving up and down which means that the device

has entered the setting mode. After that, press FUNCTION for swithing , then press "UP"and "DOWN" button again to set value which ranges in OO.OOCOST/KWH 〜 99.99COST/KWH. After setting all above, press COST to return to Mode7 or it will automatically return to Mode7 without any pressing after setting with data storage.